PolyMet Events and News

March 27, 2018

PolyMet reaffirms economic and technical viability of NorthMet Project

Highlights potential for Minnesota’s first copper-nickel-precious metals mine

St. Paul, Minn., March 27, 2018 – Poly Met Mining Inc., a wholly-owned subsidiary of PolyMet Mining Corp. (together “PolyMet” or the “company”) TSX: POM; NYSE AMERICAN: PLM – reports it has filed an updated technical report with Canadian and U.S. securities agencies that reaffirms the economic and technical viability of the NorthMet copper-nickel-precious metals project located near Hoyt Lakes, Minnesota.

The updated NorthMet Technical Report, NI 43-101, dated March 26, 2018, (“2018 Technical Report”) contains plans and cost estimates for construction and operation of the NorthMet Project. It updates a Definitive Feasibility Study originally published in 2006 and last updated in 2012 and amended in 2013 that details the economics for the mine and processing operation.

The report provides technical and economic details for development of the mining operation in two distinct phases. Phase I involves development of 225 million tons – nearly one-third of NorthMet’s known resource – into an operating mine processing 32,000 tons per day over a 20-year mine life. It also includes rehabilitating the former LTV Steel Mining Company processing plant.

Capital costs for Phase I are estimated at $945 million and include refurbishment of the existing primary crushing circuit and replacing the existing rod and ball mill circuits with a new, modern semi-autogenous grinding (SAG) mill, ball mill and flotation circuit. It also includes rail upgrades, mining equipment and a state-of-the-art wastewater treatment plant.

Phase II involves construction and operation of a hydrometallurgical plant to treat nickel sulfide concentrates into upgraded nickel-cobalt hydroxide and recover additional copper and platinum-group metals. While development of Phase II will be at the company’s discretion, both phases are currently being permitted and are included in the Final Environmental Impact Statement and draft permits. Phase II would increase the project’s capital costs by approximately $259 million.

“This report reaffirms the technical and financial viability of the 32,000 tpd case for which the final EIS and draft permits have been issued. Our focus remains on obtaining final permits under the 32,000 tpd permit case, meeting our environmental and financial assurance obligations under the terms of those permits, and obtaining the necessary financing to build the project,” said Jon Cherry, president and CEO. “We are making significant progress on all of those fronts.”

Technical Report Key Points

- Total Proven and Probable mineral reserves for the project are estimated to be 255 million tons within the pit footprint evaluated in the FEIS and draft permits, with recovered copper equivalent grade of 0.584 percent (after dilution and recoveries).

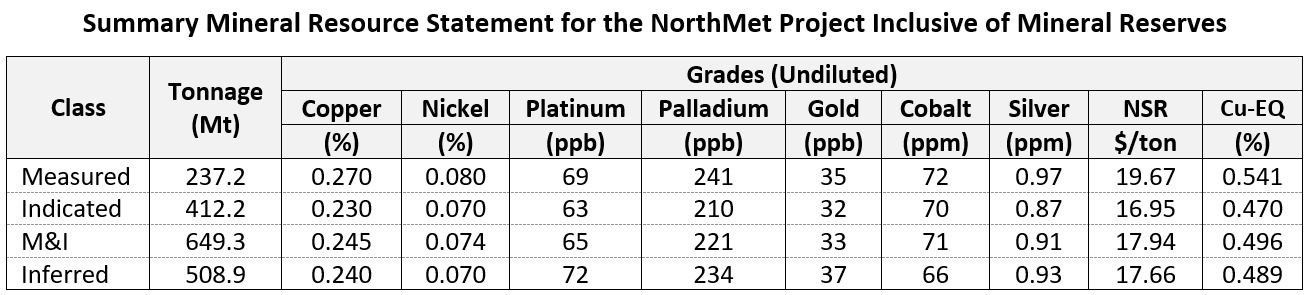

- Measured and Indicated resources total 649 million tons, with recovered copper equivalent grade of 0.496 percent.

- Inferred Resources are estimated at 509 million tons, with an estimated recovered copper equivalent grade of 0.489 percent.

- After tax, net present value of future cash flow discounted at 7 percent is $173 million for Phase I, and $271 million inclusive of Phase II.

- After tax, internal rate of return is 9.6 percent for Phase I and 10.3 percent inclusive of Phase II.

- Improvements in metal price assumptions (based on market consensus pricing) has helped offset increases in capital, operating and financial assurance expenses.

- Under Phase I, which only includes revenues based on concentrate sales, payable metals in the concentrate are estimated at 1.1 billion pounds of copper, 133 million pounds of nickel, a combined 1.1 million ounces of platinum, palladium and gold, 1.0 million ounces of silver and 5.6 million pounds of cobalt.

- Under Phase II, payable metals in enriched copper concentrates and products from the hydrometallurgical plant are estimated at 1.2 billion pounds of copper, 174 million pounds of nickel, 1.6 million combined ounces of platinum, palladium and gold, 1.0 million ounces of silver and 6.2 million pounds of cobalt. Palladium is the predominant precious metals group (PGM) product, totaling 1.2 million ounces.

A summary of PolyMet’s mineral reserves and mineral resources is provided in the tables below. Please refer to the 2018 Technical Report for important disclaimers on the viability or otherwise of reported mineral resources.

Notes:

(1) Mineral reserve tonnage and contained metal have been rounded to reflect the accuracy of the estimate, and numbers may not add due to rounding.

(2) All reserves are stated above a $7.98 NSR cutoff and bound within the final pit design.

(3) Tonnage and grade estimates are in imperial units.

(4) Total tonnage within the pit is 628,499 ktons; average waste: ore ratio = 1.47.

(5) Cu-Eq values are based on the metal prices in Table 15-2 and total mill recoveries in Table 15-3 of the 2018 Technical Report and diluted mill feed.

(6) Copper equivalent (CuEq) = ((Cu head grade x recovery x Cu Price) + (Ni head grade x recovery x Ni Price) + (Pt head grade x recovery x Pt Price) + (Pd head grade x recovery x Pd Price) + (Au head grade x recovery x Au Price) + (Co head grade x recovery x Co Price) + (Ag head grade x recovery x Ag Price)) / (Cu head grade x recovery x Cu Price).

(7) NSR values include post property concentrate transportation, smelting and refining costs and payable metal calculations.

Source: Hard Rock Consulting, LLC, January 2018

Notes:

(1) Mineral resources are not mineral reserves and do not have demonstrated economic viability.

(2) All resources are stated above a $7.35 NSR cut-off. Cut-off is based on estimated mining, processing and G&A costs. Metal Prices and metallurgical recoveries used for the development of cut-off grade are presented in Table 14-33 of the 2018 Technical Report.

(3) Mineral resource tonnage and contained metal have been rounded to reflect the accuracy of the estimate, and numbers may not add due to rounding.

(4) Cu-Eq (copper equivalent grade) is based on the mill recovery to concentrates and metal prices presented in Table 14-33 of the 2018 Technical Report.

(5) The Measured and Indicated mineral resources are inclusive of the mineral reserves.

In addition to updating the economics of the 225 million ton, 32,000 tpd case for which draft permits have been released, the report evaluates preliminary economic assessments of mining an intermediate case of 290 million tons of classified resources (96.5 percent Measured and Indicated and 3.5 percent Inferred) at a rate of 59,000 tpd, and a full-scale case that would mine 730 million tons (65.4 percent M&I and 34.6 percent Inferred) at a production rate of 118,000 tpd.

The 59,000 tpd and 118,000 tpd upside cases suggest potential valuations that range from $750 million to more than $2 billion (NPV) and IRRs that range from 18 percent to 24 percent (including both Phase I and II). The 59,000 tpd and 118,000 tpd upside cases, however, would be subject to additional engineering and environmental review and permitting. Any such opportunities would be subject to various regulatory requirements and would require additional capital investment. The included Inferred Resources would have to be successfully converted to Measured and Indicated before any prefeasibility studies could commence.

“We felt it important to quantify at a preliminary level what the potential economics of the entire NorthMet resource could be as we move forward with plans for the 32,000 tpd case,” Cherry said.

“We have already invested 13 years and more than $300 million in this project – most of that spent in Minnesota – and we are now poised to bring nearly $1 billion in new investment, hundreds of new jobs, and generate hundreds of millions of dollars in annual economic benefits for the region,” Cherry said. “We know how important this project is to the Iron Range and we have to do it right.”

For greater certainty, the preliminary economic assessments for the two upside cases referred to herein are preliminary in nature, include inferred mineral resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the results of these preliminary economic assessments will be realized. Mineral resources that are not mineral reserves do not have demonstrated economic viability and there is no certainty that mineral resources will become mineral reserves.

The NorthMet Technical Report, NI 43-101, dated March 26, 2018, was produced by Tucson, Arizona-based M3 Engineering & Technology Corporation. The report is based on detailed engineering studies as well as the Final Environmental Impact Statement and recently released draft environmental permits for NorthMet. PolyMet also retained Independent Mining Consultants, SENET, Hard Rock Consulting and Barr Engineering to contribute to the study. The report has been filed on SEDAR and EDGAR and is on the company’s website at www.polymetmining.com.

This release has been reviewed and approved by: Zachary Black, SME-RM, Hard Rock Consulting, Jennifer Brown, P.G., Hard Rock Consulting; Nicholas Dempers, Pr.Eng., SAIMM, SENET; Thomas Drielick, P.E., M3 Engineering; Art Ibrado, P.E., M3 Engineering; Erin Patterson, P.E., M3 Engineering; Thomas Radue, P.E., Barr Engineering Co.; and, Herbert Welhener, SME registered member, Independent Mining Consultants; who are all Independent Qualified Persons within the meaning of NI 43-101.

* * * * *

Investor call

PolyMet will host an investor call and webcast to discuss the updated feasibility study at 10 a.m. Central on Wednesday, March 28, 2018.

To join the call, please dial 1.877.705.6003 (U.S.) or 1.201.493.6725 (international) approximately 15 minutes prior to start time. The earnings call and slide presentation also will be broadcast live over the internet and can be accessed on the Investor Relations page of the company’s website at www.polymetmining.com.

At the time of the call, click on this link to view the presentation: http://public.viavid.com/index.php?id=128967.

* * * * *

About PolyMet

PolyMet Mining Corp. (www.polymetmining.com) is a publicly traded mine development company that owns 100 percent of Poly Met Mining, Inc., a Minnesota corporation that controls 100 percent of the NorthMet copper-nickel-precious metals ore body through a long-term lease and owns 100 percent of the former LTV Steel Mining Company site, a large processing facility located approximately six miles from the ore body in the established mining district of the Mesabi Iron Range in northeastern Minnesota. The NorthMet Final Environmental Impact Statement was published in November 2015, preparing the way for decisions on permit applications. NorthMet is expected to require approximately two million hours of construction labor, create approximately 360 long-term jobs directly, and generate a level of activity that will have a significant multiplier effect in the local economy.

For further information, please contact:

Media

Bruce Richardson

Corporate Communications

Tel: +1 (651) 389-4111

polymetcommunications@polymetmining.com

Investor Relations

Tony Gikas

Investor Relations

Tel: +1 (651) 389-4110

investorrelations@polymetmining.com

PolyMet Disclosures

This news release contains certain forward-looking statements and forward-looking information concerning anticipated developments in the operations of PolyMet in the future, including, without limitation, the statements regarding the ongoing development of PolyMet’s NorthMet Project and the results of the feasibility study on the permitted base case for the NorthMet Project as well as results of the preliminary economic assessments (PEA) on two expansion cases for the NorthMet Project. Forward-looking statements are frequently, but not always, identified by words such as “expects,” “anticipates,” “believes,” “intends,” “estimates,” “potential,” “possible,” “projects,” “plans,” and similar expressions, or statements that events, conditions or results “will,” “may,” “could,” or “should” occur or be achieved or their negatives or other comparable words. These forward-looking statements may include statements regarding PolyMet’s beliefs related to the expected project development timelines, exploration results and budgets, reserve estimates, mineral resource estimates, continued relationships with current strategic partners, work programs, estimated capital and operating costs and expenditures, actions by government authorities, including changes in government regulation, the market price of natural resources, estimated production rates, ability to receive and timing of environmental and operating permits, estimated construction costs, job creation and other economic benefits, or other statements that are not a statement of fact. In addition, and for greater certainty, the results of (i) the feasibility study on the permitted base case of the NorthMet Project, and (ii) the PEAs on the two expansion cases for the NorthMet Project constitute forward-looking information, and include future estimates of internal rates of return, net present value, future production, estimates of cash cost, proposed mining plans and methods, mine life estimates, cash flow forecasts, metal recoveries, and estimates of capital and operating costs.

Forward-looking statements and forward-looking information address future events and conditions and therefore involve inherent known and unknown risks and uncertainties. These risks, uncertainties and other factors include, but are not limited to, adverse general economic conditions, operating hazards, inherent uncertainties in interpreting engineering and geologic data, fluctuations in commodity prices and prices for operational services, government regulation and foreign political risks, fluctuations in the exchange rate between Canadian and US dollars and other currencies, as well as other risks commonly associated with the mining industry. Actual results may differ materially from those in the forward-looking statements and forward-looking information due to risks facing PolyMet or due to actual facts differing from the assumptions underlying its predictions.

In connection with the forward-looking information contained in this news release, PolyMet has made numerous assumptions, regarding, among other things, that the geological, metallurgical, engineering, financial and economic advice that PolyMet has received is reliable and is based upon practices and methodologies which are consistent with industry standards, that PolyMet will be able to obtain additional financing on satisfactory terms to fund the development and construction of the NorthMet Project and that the market prices for relevant commodities remain at levels that justify construction and/or operation of the NorthMet Project. While PolyMet considers these assumptions to be reasonable, these assumptions are inherently subject to significant uncertainties and contingencies.

PolyMet’s forward-looking statements are based on the beliefs, expectations and opinions of management on the date the statements are made, and PolyMet does not assume any obligation to update forward-looking statements if circumstances or management’s beliefs, expectations and opinions should change.

Specific reference is made to risk factors and other considerations underlying forward-looking statements discussed in PolyMet’s most recent Annual Report on Form 40-F for the fiscal year ended January 31, 2017, and in our other filings with Canadian securities authorities and the U.S. Securities and Exchange Commission, including our Report on Form 6-K providing information with respect to our operations for the three and nine months ended October 31, 2017.

The Annual Report on Form 40-F also contains the company’s mineral resource and other data as required under National Instrument 43-101.

The TSX has not reviewed and does not accept responsibility for the adequacy or accuracy of this release.